Annual inflation index for DCLs, CAC targets, and density bonus contributions

Annual inflation index for DCLs, CAC targets, and density bonus contributions

We use a Council-adopted inflationary index to keep development cost levy (DCL) rates, community amenity contribution (CAC) targets, and density bonusing rates in line with property and construction inflation.

The annual inflation index is based on a blend of property value and construction cost inflation and calculated using public, third-party data. Rates are adjusted annually through a report to Council every July, with new rates effective on September 30 of every year.

View the 2024 inflationary rate adjustments:

- Development Cost Levies and CAC Targets PDF file (928 KB)

- Density Bonus Contributions PDF file (230 KB)

| Year | Annual inflation |

|---|---|

| 2016 | 4.5% |

| 2017 | 11.9% |

| 2018 | 4.8% |

| 2019 | 5.2% |

| 2020 | -0.8% |

| 2021 | 1.2% |

| 2022 | 8.8% |

| 2023 | 8.3% |

| 2024 | 5.7% |

| 2025 | 3.2% |

Principles of the index

- Uses publicly accessible third-party data

- Transparent and replicable system

- Adjusts rates annually

- Adjusts rates upwards or downwards

- Adapts to significant market changes

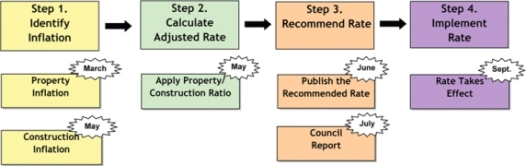

Annual index and rate adjustment process

Here are the four steps and annual timing of the index before implementation of the adjusted rates.

How the inflationary index works

Step 1 uses two main data sources:

- BC assessment net property values for the City of Vancouver

- Statistics Canada non-residential construction price index for Vancouver

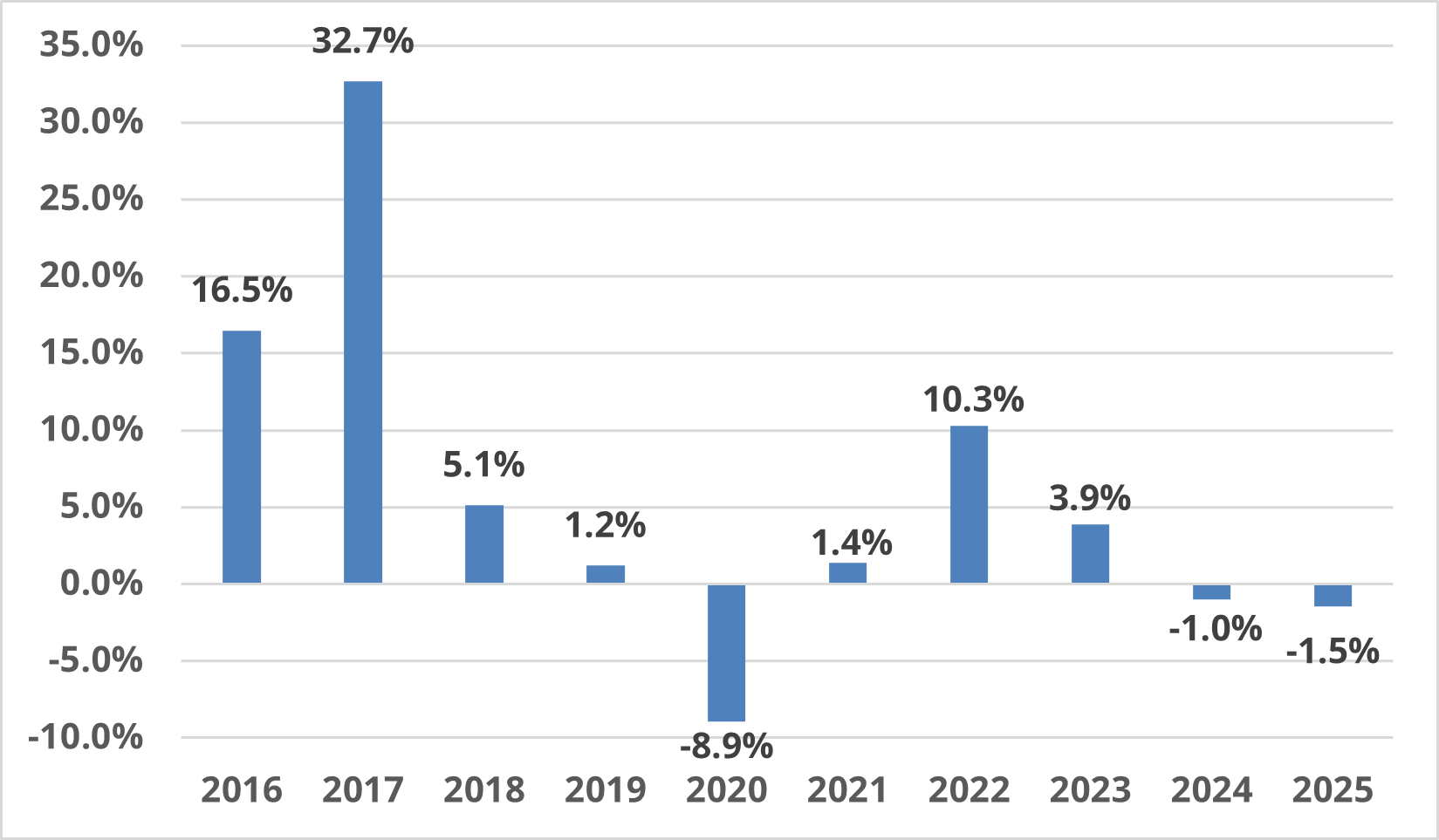

Annual Change in BCA Net Property Value for City of Vancouver - Current $

Calculated in current dollars. Property values sums all land classes and assessment areas by year. Net figures exclude exemptions.

Source: City of Vancouver Property Tax Roll, BC Assessment Authority

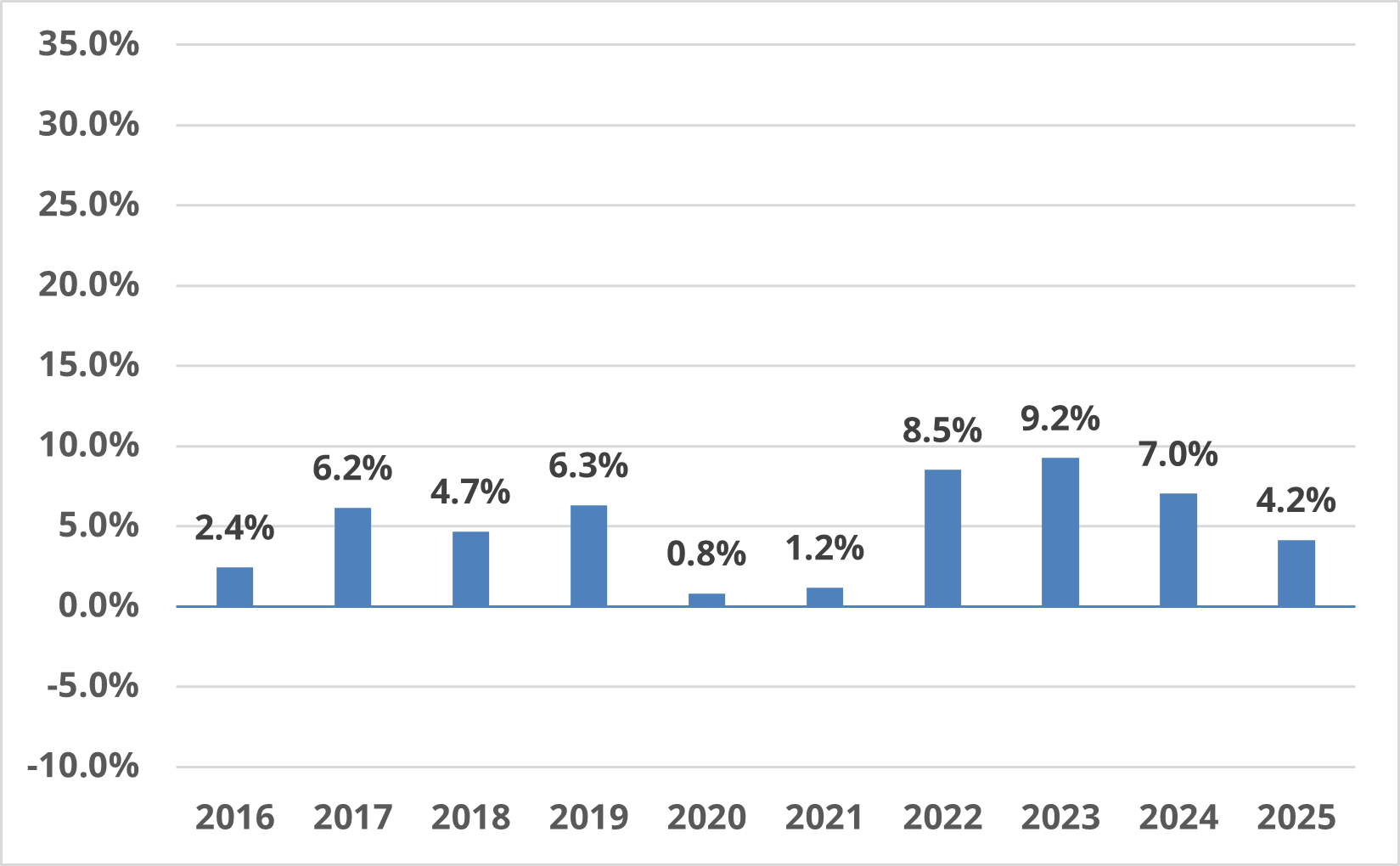

Annual Change Non-Residential Construction Costs - First Quarter Values

Reflects change in first quarter values.

Source: Statistics Canada, Non-residential construction price index for Vancouver, 2023=100.

Step 2 applies the two sources of inflationary data using the ratio of property acquisition and non-residential construction costs set out in the public benefit strategy.

Step 3 adjusts the rates, publishes for public information, and recommends the rates to Council.

Step 4 sees the new rates come into effect.

Applying the annual index and the four-step process leads to smaller, more predictable rate adjustments and responds to changes in market conditions.